College costs have risen dramatically in recent decades. Since 1989, the cost of a four-year, college degree nearly doubled after accounting forinflation. This fact, coupled with flat wage growth, recently propelled the student debt crisis to the forefront of national debate. As college tuition goes up, more and more families are applying for financial aid.

College tuition continues to climb, but so does the stock market. Diversified market exposure can accelerate savings plans and shore up future goals. Despite recent uncertainty, stocks have roared back from their lows of just a year ago. Long-term investors anticipate the inevitable fluctuations that accompany putting their capital at risk. These investors also recognize the power of compound growth.

Let’s look at a recent freshman class. Parents or relatives who invested $40,000 into a well-diversified, “moderate risk”1 portfolio at the child’s birth (2002) had over $120,000 once that child entered college in Fall 2020.2 This period includes the second-worst market crash in history – the Great Recession of 2008 – and March 2020’s sudden freefall, when the market fell nearly 30 percent in just four trading days. Disciplined investing is key to any sound college savings plan. Often overlooked is the type of investment account utilized.

Families across the country seek to get ahead of rising tuition costs, but savings strategies vary. Many parents and relatives continue to save for college the old-fashioned way, using taxable savings or brokerage accounts. Others are utilizing tax-advantaged savings vehicles such as 529 plans. Assets are factored into financial aid calculations at different rates, depending on the type of account and who owns it. Consequently, the type of savings vehicle that you choose can have a huge impact on financial aid eligibility.

Families must coordinate college savings strategies with an increasingly complex financial aid system. This article will guide families toward a prudent college savings plan that seeks to optimize both savings growth and financial aid eligibility.

College Savings

Complicated and, at times, counterintuitive financial aid calculations leave many families wondering how they should save for college. College saving and prudent asset structuring go hand-in-hand. Families that begin preparing for college early can invest for long term growth. However, it can be easy to unknowingly compromise financial aid eligibility prospects in doing so.

The advent of tax-advantaged savings vehicles further complicates the financial aid process. It can be difficult for families to coordinate savings goals with future financial aid objectives. Assets count toward financial aid calculations at different rates, depending on the type of account and who owns it. It is critical that families use the right savings vehicle.

Enter state-sponsored 529 savings plans. 529 plans are advantageous for three reasons. Firstly, 529 plans enjoy high aggregate contribution limits and no income eligibility requirements.3 Virtually anyone can contribute any amount. Secondly, while contributions are not deductible for federal income tax purposes, 529 assets grow tax deferred and qualified withdrawals for educational expenses are tax-free. Lastly, and perhaps least understood, 529 plans reduce financial aid eligibility only minimally compared to other savings accounts.

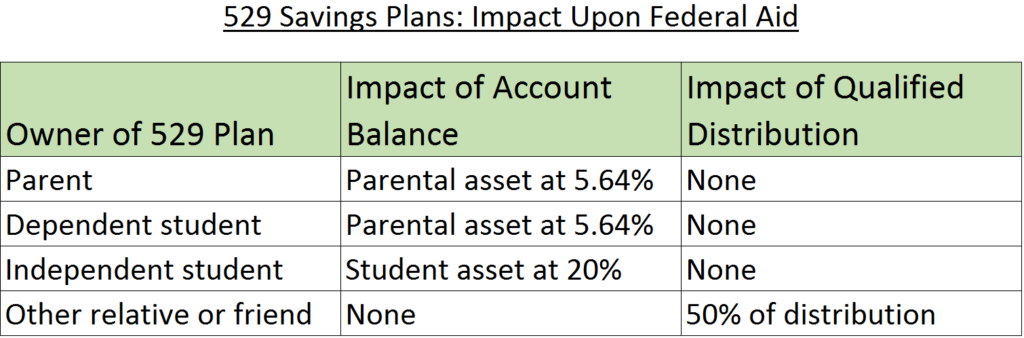

529 plans allow parents, relatives, and even friends to contribute substantial amounts on behalf of a child’s college education.4 However, only 529 plans owned by the parent or dependent child benefit from minimal FAFSA consideration. Up to 5.64 percent of a parent or student owned 529 plan is included in the “Expected Family Contribution.” 529 plans owned by friends or other relatives are subject to significantly higher FAFSA assessment rates (See Table).

Families must complete an additional form, called the CSS Profile, to apply for institutional aid dollars. 529 plans are assessed similarly for this purpose. We encourage parents to check with individual colleges regarding how the plan assets will be assessed. Your safest bet is to open a 529 plan in a parent’s name if you are unsure.

The good news is that anyone can pitch into a 529 plan. Relatives and friends can fund a parent or child-owned 529 plan without jeopardizing future financial aid eligibility. We always recommend establishing 529 plans under the parent or dependent student’s name, even if the plan will be funded by someone else.

We encourage families to carefully review various 529 investment options. Families should select a portfolio that is coordinated with the child’s projected college timing. In other words, investment risk should be reduced as the child approaches college age. Most states offer their own 529 plans with various investment options. Nearly all 529 plans are relatively low cost and provide ample diversification across stocks and bonds. Certain 529 plans also offer state income tax deductions to in-state residents, though families are free to use an out-of-state 529 plans instead. Scrutinize investment options, tax advantages, and costs when evaluating plans.

529 Plan Flexibility

The most overlooked benefit of the 529 plan is flexibility. Qualified 529 distributions are not restricted to college tuition payments. Other college-related expenses, such as off-campus housing, textbooks, and computer software may also qualify. Perhaps more significantly, 529 plans may also be used to fund private elementary and high school educations.

Surely, funding a 529 plan is a major commitment. What happens if the beneficiary chooses to forego a college education? Families need not fret. Recent legislative changes render certain Labor-Department-registered apprenticeship programs eligible for 529 funding. 529 assets can also be allocated to vocational and trade school costs.

Federal guidelines also allow you to transfer funds from one beneficiary to another family member with ease. Qualified family members include siblings, children, first cousins, and even nieces and nephews. Be mindful, however, that each beneficiary is only allowed one tax-free 529 rollover per twelve-month period.

Moreover, with the passage of the SECURE Act (2019), families can use 529 funds to pay up to $10,000 toward student loans in the name of the plan’s beneficiary or a beneficiary’s sibling. This presents two potentially advantageous strategies. Firstly, families might avoid using 529 funds – at least initially. Instead, these families could take out low-interest loans for the child’s education, prolong tax-free investment growth, and pay back these loans with 529 funds at a later date. The second strategy applies to situations in which one child attends a cheaper college than his or her sibling. Remaining 529 funds may be used to pay student loans already taken on behalf of the other child’s more expensive tuition.

Lastly, tuition payments can be coordinated with available tax credits. The American Opportunity Tax Credit and the Lifetime Learning Tax Credit provide thousands of dollars in tax credits for qualified educational expenses, though there are two important caveats.5 These credits may not be claimed together in the same year for the same student. In addition, the IRS forbids families from claiming either tax credit on 529 withdrawals. Well-heeled families, however, can effectively “double-dip” by paying a portion of tuition expenses from non-529 assets and claiming tax credits on these dollars. Remaining educational costs can then be covered from 529 accounts. A personalized tax analysis is necessary to determine whether this strategy is worthwhile.

529 plans are a versatile, tax-advantaged savings vehicle for your child’s future. As tuition rates continue to rise, families increasingly ponder the value of a traditional college degree. These skeptics can be assured that 529 plans are advantageous whether the beneficiary attends a four-year college or chooses an alternative route. Families can also shift 529 funds to where they are most needed as individual educational goals become clearer.

Alternative Savings Plans

College saving is a very unforgiving process. The unfortunate reality is that many people choose the wrong savings vehicles for college expenses. Coverdell Education Savings Accounts (ESAs), for example, function very similarly to 529 plans. Coverdell ESAs allow tax-free withdrawals for qualified educational expenses. However, these accounts are subject to an annual contribution limit of $2,000 per child, which severely restricts a family’s ability to save. Participation in Coverdell ESAs is limited to individuals earning below $110,000 per year or married couples earning below $220,000 per year.

Other families make the mistake of funding a Uniform Transfer to Minors Act (UTMA) account for their child’s college education without considering alternatives. A UTMA is set up for the named benefit of a minor and managed by a parent or trusted fiduciary until the child reaches age 18. UTMA savings, like all custodial assets, are counted at a 20 percent rate by FAFSA when determining a family’s financial aid. 529 plans are far preferable to families seeking financial aid.6

Another savings vehicle further complicates college savings strategy – prepaid tuition plans. Prepaid plans enjoy the same tax benefits and FAFSA assessment rates as 529 savings plans. These plans allow investors to pre-pay for college costs at today’s tuition rates. Prepaid plans then translate contributions into tuition contracts or credits, which can later be redeemed at participating institutions. While these plans effectively hedge rising tuition costs, several caveats exist. Notably, state-offered prepaid tuition plans typically limit eligibility to in-state residents.7 Furthermore, prepaid plans cover tuition and fees only, while conventional 529 plans cover a long list of related expenses. Lastly, prepaid funds may be subject to penalty if your child attends a non-participating college. Prepaid 529 plans offer many advantages, though investors must scrutinize the inherent risks before proceeding.

Flexible participation rules, high contribution limits, and favorable FAFSA assessment make conventional 529 plans hard to beat. Families that already funded a Coverdell ESA or UTMA can roll assets to a 529 savings plan with ease. Unfortunately, prepaid tuition rollovers may be subject to state income taxes and an additional penalty. Applicable families should contact a trusted financial planner to evaluate and facilitate 529 rollovers.

Takeaways

Saving strategies represent a key component in the college planning equation. 529 plans are a terrific tax-advantaged investment vehicle for families that want to save for college and maximize financial aid eligibility.

A sound college savings plan will prioritize discipline, cost-effectiveness, and tax mitigation. Furthermore, families should carefully weigh the inevitable trade-off between risk and return. Households that begin saving for college early can pursue an aggressive investment plan while the child is young. Families that begin saving later may be forced to sacrifice growth potential by adopting a more conservative investment approach.

Families typically confront competing financial goals while their children are young. Child costs, retirement saving, and short-term spending objectives can deter the most sophisticated investors from saving for college. Unfortunately, many families forfeit the opportunity to build an educational nest egg. Compound growth is irretrievable once the time has passed. Start small, begin early, and take advantage of long-term appreciation. The adage that a little goes a long way certainly applies here.

The college debt situation is surely out-of-hand and tuition rates continue to soar. Fortunately, careful planning can dampen this burden. We encourage families to research state-offered 529 plans online. Alternatively, investors may simply contact a competent financial planner who will evaluate anticipated educational needs, advise 529 plan selection, and guide funding strategies. There is no better time than now.

AIS can provide college planning guidance and financial aid eligibility analysis at any time. Please contact Bryce Schuler at 413-591-4448 or BryceS@americaninvestment.com for a complimentary educational planning review.

- The AIS “moderate risk” portfolio is composed of 60% stocks, 35% bonds, and 5% gold. Investment vehicle recommendations can be found on the back page of each month’s Investment Guide.

- Sample portfolio statistics are hypothetical and do not reflect historical recommendations of AIS. Annual portfolio rebalancing is assumed.